“Social inflation” refers to the impact of rising litigation costs on insurers’ claim payouts, loss ratios, and, ultimately, how much policyholders pay for coverage. While there’s no universally agreedupon definition, frequently mentioned aspects include:

“Social inflation” refers to the impact of rising litigation costs on insurers’ claim payouts, loss ratios, and, ultimately, how much policyholders pay for coverage. While there’s no universally agreedupon definition, frequently mentioned aspects include:

- Proliferation of class-action suits and other lawyer- and government-driven actions (“runaway litigation”);

- Growing awards from sympathetic juries (“nuclear verdicts”);

- “Litigation funding” – in which investors finance lawsuits against large companies in return for a share in the settlement; and

- Rollbacks of tort reforms that were intended to control costs.

Is it real? The research says, ‘Yes!’

Some have questioned its existence and derided it as a “hoax.” But recent research by Triple-I, in partnership with the Casualty Actuarial Society (CAS), and the Insurance Research Council (IRC) confirm and quantify the phenomenon.

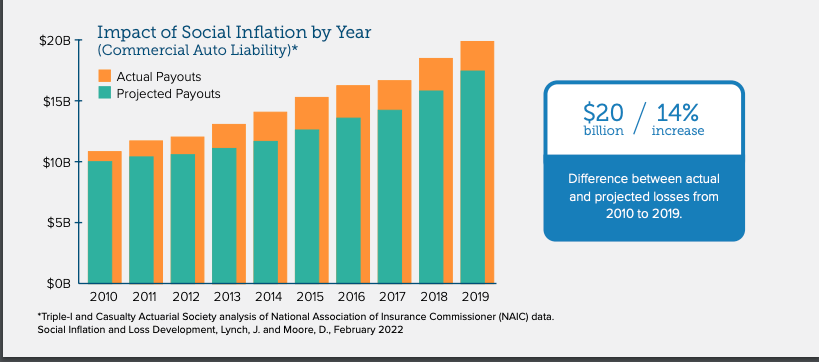

The Triple-I/CAS paper found that social inflation increased claims for commercial auto liability alone by over $20 billion between 2010 and 2019. It also identified evidence of similar trends in other lines, such as “other liability occurrence” and claims-made medical malpractice.

A separate IRC paper illustrated how losses across several insurance lines have accelerated in recent years much faster than economic inflation alone can explain.

“It is not unusual for premiums for a smaller [trucking] fleet to rise 50 to 100% or more in any given year. The inflation of trucking insurance rates makes healthcare inflation (which makes endless media headlines for being out of control) look downright paltry in comparison.”

– Seth Holm of FreightWaves, a transportation industry website. Trends and Insights: Social Inflation: What it is and why it matters “

Commercial trucking is among the sectors most severely affected by more frequent lawsuits generating higher penalties. A 2020 study by the American Transportation Research Institute found that, from 2010 to 2018, the size of verdict awards grew 33 percent annually, as overall inflation grew 1.7 percent and healthcare costs grew 2.9 percent.

More frequent suits and bigger awards can lead to increased insurance costs as rates are adjusted to reflect the changing risk profile – or even to insurers ceasing to write particular forms of coverage. Higher premiums tend to be passed along to consumers in the form of higher prices and, in extreme cases, can ripple through the entire economy, creating conditions analogous to the 1980s liability crisis.

Drivers of Social Inflation

Cultural attitudes:

The “social” part of the name speaks to shifting public perceptions and attitudes, such as negative sentiment toward corporations and desensitization to large jury awards. Greater awareness of CEO salaries and a growing wealth gap may lead jurors to sympathize with plaintiffs when awarding damages because it is perceived that the business or its insurer “can afford it.”

These shifts make it easier for plaintiff attorneys to use “reptile theory” to influence juries. Introduced in the book Reptile: The 2009 Manual of the Plaintiff’s Revolution, the idea is to use jurors’ emotions and fears to evoke sympathy for plaintiffs by appealing to the primitive part of the human brain shared with reptiles.

Litigation 2.0:

Emotional appeals by plaintiffs are nothing new. Neither are class action lawsuits. But the plaintiff bar has gone to a new level with tactics like third-party litigation funding and litigation lending. Funding of lawsuits by international hedge funds and other financial third parties – with no stake in the outcome other than a share of the settlement – has become a $17 billion global industry, according to Swiss Re. Law firm Brown Rudnick sees the industry as even larger, at $39 billion global industry in 2019, according to Bloomberg.

“It’s being used to fund everything from Russian oligarchs’ divorces to take on banks in fraud suits,” Bloomberg writes.

Some funders have gone further, and now a tech start-up is looking to gamify third-party litigation funding by facilitating online buying and selling of lawsuit shares.

“It’s kind of like litigation financing, but on steroids,” writes Mark Dubois, an attorney and former chief disciplinary counsel for the state of Connecticut. “The projected returns on investment are huge.

The legal profession has become concerned about the ethics of such arrangements. In 2020, the American Bar Association (ABA) approved a set of best practices for litigation funding. The resolution recommends that lawyers detail all arrangements in writing and advises them to ensure that the client – not the funder – retains control.

Some states have begun requiring disclosure of thirdparty funding. Such efforts predictably meet resistance from commercial litigation funders. In 2020, the 13 largest commercial litigation funders in the world formed the International Legal Finance Association (ILFA) to advocate for litigation funding and oppose blanket disclosure requirements. According to its website:

“The use of legal finance in a private action by a commercial client is a private matter that should not be disclosed to anyone.”

Back to the future?

In the 1980s, liability claims were pushing the U.S. insurance industry to the brink of collapse.

“It was not just doctors facing expensive litigation claims for medical malpractice who found it increasingly difficult to get cover,” writes SwissRe. “Liability insurance costs for teachers, fire brigades, police officers and many other professions skyrocketed also.”

Juries of laypeople, even in complex cases, determined liability and awarded punitive and “pain and suffering” damages. Contingency fees of about 30 percent for lawyers provided incentives that caused the practice to get out of hand. Loss ratios soared, and insurer insolvencies became commonplace.

Tort reforms – ranging from capping non-economic damages and limiting contingency fees to specifying statutes of limitations and eliminating “joint and several” liability – were enacted, and losses declined. It has been argued that legislative efforts to roll back these reforms in many states have contributed to social inflation, but the research is not conclusive.

Originally posted on Insurance Information Institute

Blog