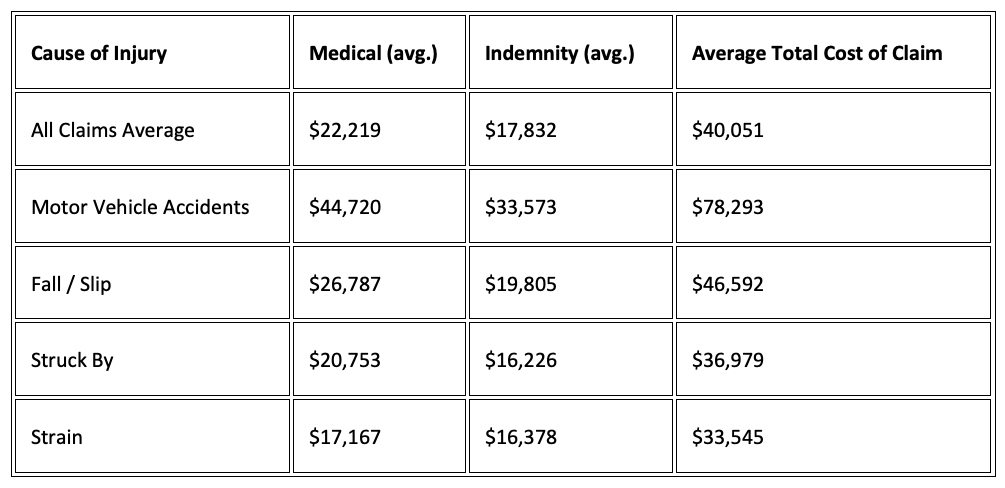

For most employers in the United States today, mitigating workers compensation claims is a key component of a company’s overall cost management strategy. Rightly so – the actual costs of a single workers compensation claim can be staggering (see table below for some of the most common and costly types of claims).

For most employers in the United States today, mitigating workers compensation claims is a key component of a company’s overall cost management strategy. Rightly so – the actual costs of a single workers compensation claim can be staggering (see table below for some of the most common and costly types of claims).

According to the National Safety Council, the average cost of workers compensation claims is $40,051.

One of the best ways to approach workers compensation is changing the light you view it in. Rather than seeing it as a necessary evil, try viewing it as an integral and beneficial part of your health care, disability, and lost wage benefit program.

Studies have found that when you take a holistic, multidisciplinary approach to your employees’ health, you can lower claims across the board for all employee-health-related programs.

How are workers compensation and health care, disability, and lost wage benefits connected?

Workers compensation and health care, disability, and lost wage benefits are all different facets centered on your employees’ health — a claim in one program often leads to a claim in another.

When employees have chronic conditions, unhealthy behaviors, or poor health, there’s often an increase in all employee-health spending and job downtime. In case you needed it confirmed further, here are some facts and statistics about employee health.

- 90% of the nation’s $4.1 trillion in annual health care expenditures are for people with chronic and mental health conditions.

- Debilitating chronic health conditions, such as musculoskeletal disorders, can arise from on-the-job injuries. Examples of musculoskeletal disorders include persisting back pain, back injury, hernias, sprains/strains, tears, etc.

- Chronic conditions can arise unexpectedly after an on-the-job incident and are often exacerbated by comorbidity factors such as obesity or diabetes. These unexpected developments place a strain on employer resources.

- When an employee has an existing chronic health condition (obesity, diabetes, arthritis, asthma, hypertension), they are more likely to develop another chronic health condition. Generally, the more chronic health conditions an employee has, the longer the recovery time they face after injury.

How do I mitigate employee health costs?

You can’t control your employees’ lives or keep them contained in bubble wrap at all times. However, you can provide employees with education and resources that help them understand the risks posed by chronic health conditions in both their work and everyday lives. You may also be able to implement improved workplace safety procedures.

That said, while risk reduction measures and protocols are undoubtedly important in their own right, especially in high-risk industries, they often miss the mark in terms of addressing some common triggers of workers compensation utilization.

Other factors that may contribute to claim incidences across all industries include:

- High level of turnover: High turnover means frequently bringing on new employees. One workers comp underwriter analyzed five years of claims and found that 28% of workplace injuries resulting in claims happened in the first year of employment.

- An aging workforce: Though older and more experienced employees are injured less often than their younger peers, the claim costs of your aging workforce are often higher, and the time they spend away from work while recovering is longer.

- Stress factor: High levels of stress impact people negatively. Stress can also lengthen recovery time, which in turn impacts claim costs. You can’t fix an employee’s circumstances, but you can give them more control over their work schedule and benefit options.

Accident and Disability Benefits

One strategy that has emerged as an effective and proactive approach to controlling workers compensation claims is offering accident and disability benefits to employees. A study by Aflac found that 42% of all companies providing access to voluntary accident and disability insurance experienced declines in their workers compensation claims. Both plans can be designed to provide benefits that are paid directly to employees — only for non-occupational injuries and illnesses — consequently helping to eliminate “Monday morning claims.”

Offering voluntary benefits such as accident and disability insurance at the workplace has also been linked to increased employee attraction, retention, and loyalty, which can help alleviate high turnover rates – another common trigger.

42% of all companies providing access to voluntary accident and disability insurance experienced declines in their workers compensation claims.

An Attractive Option

On a voluntary basis, there is no direct cost to employers for offering these benefits, making it an attractive option for those looking to control costs while enhancing their benefits offering at the same time. The key to any successful voluntary program is having a strong communication and education campaign to ensure employees understand, value, and utilize the benefits. In light of the cost savings on their workers compensation rates and given the affordable nature of these benefits, an increasing number of employers are also opting to include these benefits as a part of their employer-paid total benefits package.

Offering accident and disability benefits to employees is a proactive approach to effectively mitigate all employee-health-related claims by addressing some of the common triggers for utilization. These benefits provide employees with the financial protection they need in the time of an injury or illness.

Contact your Webber Advisors insurance advisor to learn more about accident and disability benefits and find out if this is a good option for your organization.

References

- https://injuryfacts.nsc.org/work/costs/workers-compensation-costs/

- Naumann, Michael (2015, Oct 30). Voluntary A&D Insurance May Reduce Workers’ Compensation Claims. Property Casualty 360

https://www.propertycasualty360.com/2015/10/30/voluntary-ad-insurance-may-reduce-workers-compensa/ - Burdick, Guy (2019, Jun 26). The Root Causes of Workers Compensation Claims. EHS Management https://ehsdailyadvisor.blr.com/2019/06/the-root-causes-of-workers-compensation-claims/

Blog